{kind=link}

As a species, human beings like to compete with each other. I see this aggressive nature on show day by day with my six-year-old James and nine-year-old Max. Who can stand up the steps first? Who can end their dinner first? Who will get to cuddle with daddy first? (Okay, full disclosure right here, it’s normally a battle over who can cuddle with mommy!) Profitable, doing higher than another person, and outperforming are in our blood. In some ways, this idea additionally applies to analyzing your portfolio’s funding efficiency. However to precisely decide outperformance, it’s necessary to match your outcomes in opposition to the right normal or benchmark.

What Is Profitable?

The opposite day after Max’s baseball recreation, James (filled with liquid braveness from consuming his blue slushy) challenged me to a race across the bases. Not being from the “participation trophy period” of right this moment, I went full out and handily beat him. Now, my mates typically joke that my legs are so skinny that folks would possibly chalk them up if I handed a pool corridor. Nonetheless, it was not a “truthful” race, as my legs are for much longer and my physique is extra developed than my son’s. (I be previous!) In fact, if James have been to run in opposition to children who have been nearer to his age, it could present a significantly better litmus check of how briskly he actually is.

The identical thought holds true for evaluating the efficiency of your portfolio. Typically, advisors request that I take a second take a look at a portfolio when shoppers ask about their returns in contrast with “the market.” For many buyers, the market refers back to the S&P 500. For probably the most half, this index consists of large-cap U.S. fairness. So, until you personal a equally constructed portfolio, it’s not a good comparability.

As an alternative, a extra acceptable benchmark is a blended index that features the Russell 3000 (home fairness), the MSCI World ex-U.S. (worldwide fairness), and the Bloomberg Barclays U.S. Mixture Bond (bonds) indices, in addition to money. As well as, the proportion in every index ought to mirror a shopper’s precise allocation to home equities, worldwide equities, bonds, and money. To “win,” shoppers ought to consider whether or not their investments beat this blended benchmark.

Everyone Need to Rule the World

The above references a music from 1985 by Tears for Fears. It falls outdoors my high 1,000 favourite songs; nonetheless, it does communicate to how the typical investor needs to make as a lot because the market, so long as the market is up. It’s also completely regular to have a short-term reminiscence and overlook that the S&P 500 was down 37 % in 2008. Advisors work with shoppers to find out their threat tolerance and, in flip, the asset allocation that aligns with it. The extra threat that you’re prepared to tackle, the higher the chance that your return might be greater due to it. Conversely, with greater threat comes a better likelihood of extra lack of principal when the market falls.

What Goes Round, Comes Round

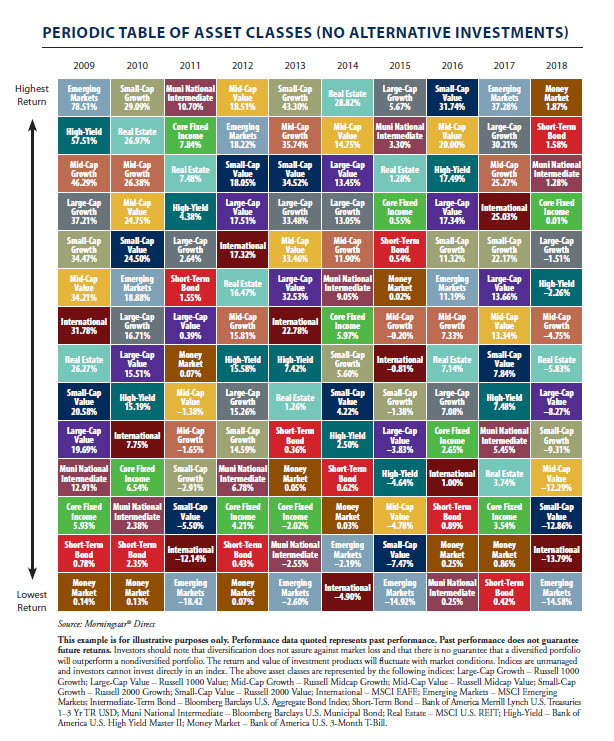

This brings us to the idea of diversification. With hindsight, it’s not uncommon for an investor to assume, “why didn’t my advisor simply put all my cash into Amazon and Apple?!” Cue the reference to the dot-com bubble of 2000 that I witnessed firsthand as a inventory dealer. Now, I’m not saying that right this moment’s tech giants are analogous to people who crashed like Pets.com. However Newton’s regulation of gravity of what goes up should come down applies right here. How a lot they go down is one other story. The purpose is one thing that has been continuously emphasised with all buyers: diversification is important to long-term efficiency. Just like the circle of life (the brand new Lion King now enjoying in a theater close to you!), an asset class can do nice one yr and horrible the following. As an illustration, rising markets fairness was up 37.28 % in 2017 and down 14.58 % in 2018. The Callan chart under illustrates this idea greatest.

A Marathon . . . Not a Dash

Again in 2000, I made a decision to run the Boston Marathon although I had by no means run greater than 5 miles at a time in my life. Formed extra like a rhombus than a runner, I spotted that the one approach that I might run 26.2 miles could be to run comparatively sluggish and steadily construct up my endurance. Within the quick run (pun meant!), my tortoise-like tempo saved me at the back of the pack. In the long term? I used to be in a position to endure and end the race, whereas others that have been as soon as forward of me fell by the wayside. I had achieved my purpose.

Investing will be checked out in the identical gentle. It’s about engaging in your purpose, whether or not that is proudly owning a house, placing your children by means of school, or retiring at a sure age. You’ll be able to solely dash for thus lengthy. The previous adage of sluggish and regular wins the race applies right here.

The Backside Line

I educate my boys that it’s okay to be aggressive however that it’s also okay to lose. Each, in the long term, will make them stronger and assist them obtain their objectives in life. They need to measure their relative success or failure in opposition to acceptable benchmarks. Buyers would do effectively to do the identical.

Editor’s Word: The unique model of this text appeared on the Impartial Market Observer.